We are being forced into a cashless society by two powerful forces – the banks (seeking more money) and the government (seeking more control).

Cash is reliable, surcharge-free, and private. It is also tangible – so handing over money and receiving some back makes you think a bit more about what you are spending. Cash also allows you to track your spending; if you take $200 out at night, you know how much you have spent at any point in time by just seeing how much cash is left.

There is no alternative to cash and it is important that it is kept, because once it’s gone it’s gone for good.

The method being used to make our society cashless is by limiting our access to cash. If we can’t get cash, then we can’t spend cash. As detailed in Australia’s ATM extinction!, the number of ATMs has been in rapid decline since the banks stopped making money from them – 14,000 bank-owned ATMs to 5,500 in seven years.

Blind Freddy could see what would happen when the $2 fee for non-bank customers ceased, yet vacuous politicians cheered the move with then-Treasurer Scott Morrison even claiming the move came after pressure from the government. Thanks for nothing, Scott.

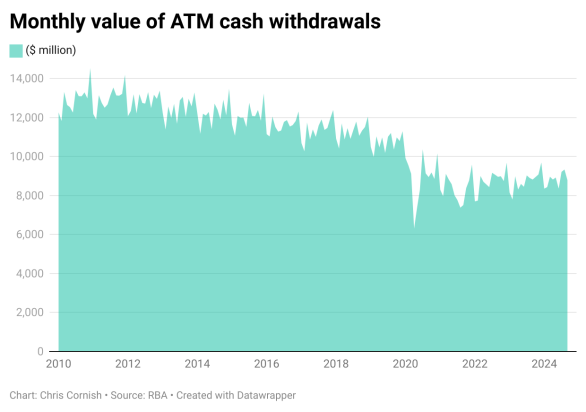

When coupled with ongoing branch closures, cash has never been harder to come by and this forced reduction in cash usage is then used to promote the falsehood that we as a society no longer want to use cash. But it is clear there is still strong demand for cash. The latest RBA figures show that $8.79 billion was withdrawn from ATMs in September 2024 alone.

There are two main reasons the banks want us in a cashless society. The first is that cash is expensive for them to maintain. Filling up ATMs and dispensing cash at branches comes at a cost. The other reason is the money they make from alternate payment methods.

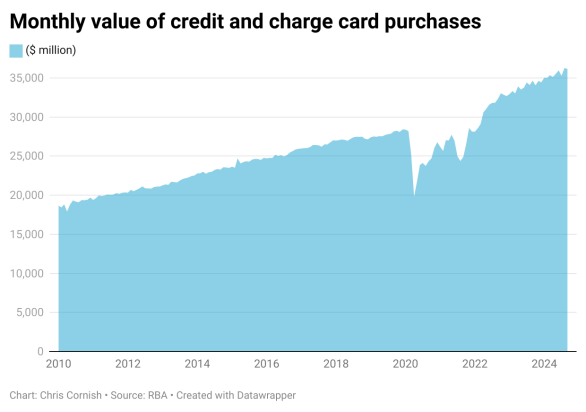

Credit and charge card spending is now $36 billion per month, 28 per cent higher than pre-pandemic levels. That’s a lot of extra banking fees for the banks.

You’d be forgiven for thinking that the surcharge fee goes straight to the two main card providers, Visa and Mastercard, but this is not the case. The surcharge ‘include costs such as merchant service fees, terminal fees, and any other fees incurred in processing card transactions’ (RBA), and it is the banks who profit handsomely from these components. As well as some merchants who make the most of the latitude given to them – it is fairly simple to make a case that the majority of your business banking costs can fall under ‘other fees incurred in processing card transactions’. In addition, I have personal experience where the banks themselves have sought to exploit this situation. When I was a Councillor at a local government, and Chair of the Audit and Risk committee, we decided to review the city’s banking arrangements. A Big 4 bank offered us lower organisational banking fees if we opted for a higher credit card fee (which we could then make surchargeable). I suspect it is quite common for the surcharge to be used to offset non-related banking costs.

I sympathise greatly with small business and know how banking fees add up, especially for retailers. Whilst Europe, Malaysia, and the UK have banned credit card surcharges, I don’t seek that. But equally, I don’t think it acceptable for a price to be advertised, and then an unknown surcharge to be added on that good at the till. Especially if you have committed to that purchase by having eaten the food, or filled your trolley. So the transparency and consistency of these fees need to be greatly improved.

Ideally, the banks themselves need to come under the microscope, along with the fees they’re imposing on merchants.

So what is the government doing?

The government know that Australians are now paying approximately $1,000,000,000 in surcharge fees, and that it’s becoming harder to avoid these fees due to the disappearing bank branches and ATMs.

To their credit, in October they initiated a review by the RBA on the feasibility of banning surcharges on debit card transactions. If this does eventuate though, it is predictable that there will be a cost shift from the banks and retailers, and more fees will just be allocated under credit cards rather than debit cards.

The government has also announced a move towards mandating cash acceptance for essential purchases like fuel and groceries. However the details are far from final and it can be assumed that there will be ultimately be plenty of exemptions. And why is it just for essential items?

Whilst the proposed cash mandate for necessities is a welcome (baby) step, it fails to ignore the fundamental problem of cash accessibility. The banks continue to make accessing cash difficult, and now costly. Commonwealth Bank have just announced a $3 withdrawal fee for customers withdrawing cash from branches. And as night follows day, so too will the other banks likely follow this signal given to them by the CBA.

What is required from the government is to mandate cash accessibility. A determination needs to be made on how many ATMs are required to service Australia, and then everyone with a banking licence should help fund that ATM network. The actual level of funding can be proportioned on a metric such as customer numbers, net profitability or similar.

It is clear the community want cash to continue, and if we can access it we will continue to use it. The government’s current actions do not address the core issue – cash accessibility. Until they are forced to act in a meaningful manner by the voting public, we will continue this move towards a cashless society.